The sharp repricing of oil introduced a broad cost shock across energy‑intensive sectors, with road transport particularly exposed.

For a country where freight activity is overwhelmingly road‑based, higher fuel prices are transmitted directly into supply chain costs, distribution margins, and ultimately consumer prices. This dynamic is now reshaping the environment in which the automotive industry operates.

Although inflation was still relatively contained at 3.1% year‑on‑year in March 2026, this figure preceded the full impact of the fuel price surge. The April consumer price index, due in May, is expected to capture these effects more comprehensively, with forward‑looking indicators pointing to a meaningful acceleration in inflation over the coming quarters.

Fuel and transport costs are set to act as the primary transmission channels, placing strain on household budgets and business operations alike. At the same time, the monetary policy outlook has shifted materially, with market expectations moving away from further easing and towards a more cautious stance in response to inflationary risks.

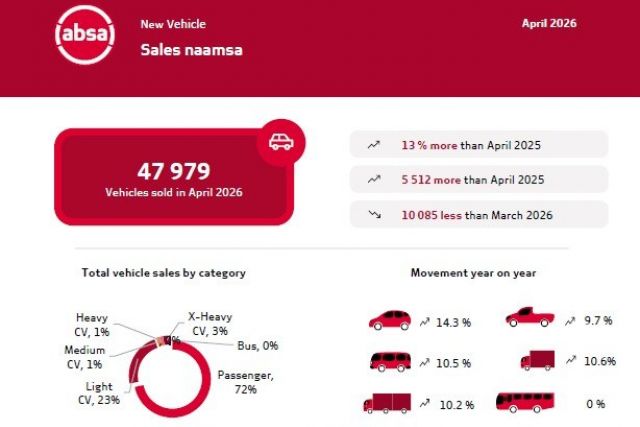

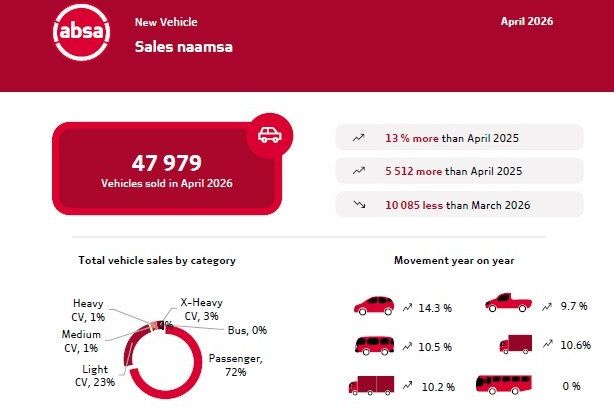

Against this backdrop, South Africa’s new vehicle market demonstrated resilience in April. Domestic demand continued to anchor industry activity, even as external shocks weighed on exports. Aggregate domestic new vehicle sales reached 47 979 units, the strongest April performance since 2013. This represented an increase of 13.0% compared to the 42 467 vehicles sold in April 2025.

Passenger cars led the way, with 34 414 units sold, up 14.3% compared to the same month last year. Car rental sales made up 5.7% of this segment, reflecting steady demand from tourism and business travel.

Exports, however, remained under strain. Vehicle export sales fell to 30 939 units, a decline of 4.0% compared to April 2025. The contraction was driven largely by the light commercial vehicle segment, which dropped sharply by 42.9% due to the phased rollout of new‑model production by a key exporter. Broader geopolitical developments and their impact on destination markets also weighed on performance.

One crucial factor supporting domestic resilience has been the extension of temporary fuel levy relief announced on 28 April. The measures include the continuation of the R3.00 per litre petrol levy reduction until 2 June, an additional 93 cents per litre diesel levy relief for May that effectively reduces the diesel levy to zero, and a phased withdrawal beginning in June before a full return to statutory levels in July.

The decision to reduce the diesel levy to zero carries particular significance for the commercial vehicle segment. Medium and heavy trucks, central to freight, infrastructure delivery, and logistics, are highly sensitive to fuel costs, which constitute a primary component of operating expenditure. Nevertheless, the relief measures are temporary and cannot fully offset the broader impact of structurally higher oil prices.

More results here.