VW celebrated top dealers and top motoring groups

CFAO‘s Mc Duling Motors under the leadership Allan Stiles as Dealer Principal scooped the top award as Dealer of the Year at VW’s recently held Grand Prix Awards.

- Dealer News

- 5 May 2026

The positive momentum of new vehicle sales in 2025 seems set to continue in 2026, with January building on the previous year’s success, says the Automotive Business Council (naamsa).

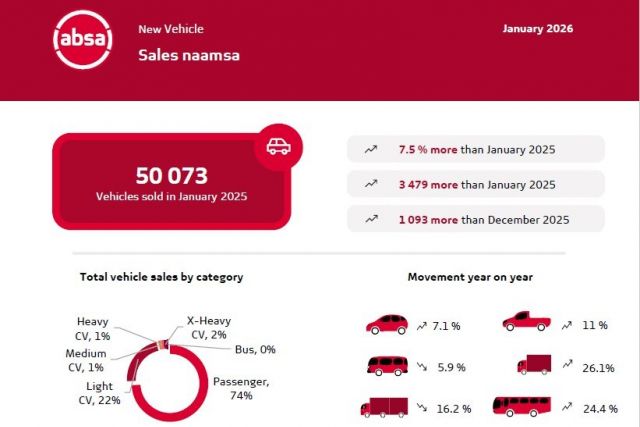

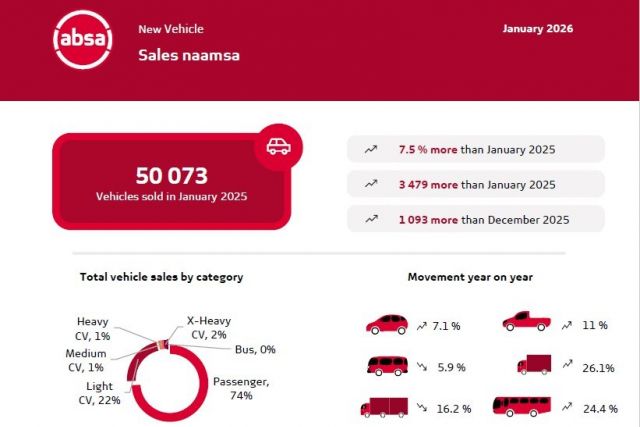

Aggregate domestic new vehicle sales in January 2026, at 50 073 units, reflected an increase of 3 479 vehicles, or a gain of 7,5%, compared to the 46 594 units sold in January 2025. Export sales rose to 24 568 units, representing a gain of 136 vehicles, or 0,6%, compared to the 24 432 units exported in January 2025.

Naamsa notes that the January 2026 performance reflects not merely a carry‑over or base effect, but a material improvement in underlying demand conditions, supported by moderating inflation, stable macroeconomic variables, and a resilient consumer base.

Of the total reported industry sales of 50 073 vehicles, an estimated 42 753 units, or 85,4%, represented dealer sales. Approximately 10,9% went to the rental industry, 2,1% to corporate fleets, and 1,6% to government.

The January 2026 new passenger car market at 37 190 units recorded an increase of 2 480 vehicles, or 7,1%, compared to the 34 710 cars sold in January 2025. Car rental sales accounted for 13,3% of new passenger vehicles sold during the month. Domestic sales of new light commercial vehicles (bakkies and mini‑buses) at 10 996 units recorded an 11% increase compared to the 9 903 units sold in January 2025. Naamsa observed that demand for light commercial vehicles continues to track broader conditions in the goods‑producing sectors of the economy, which remain constrained but show signs of gradual stabilisation.

Sales in the medium and heavy commercial vehicle segments reflected weaker performance in January 2026. Medium commercial vehicle sales at 542 units represented a 5,9% year‑on‑year decrease, while heavy trucks and buses at 1 345 units reflected a 4,3% decline compared to January 2025. Fleet replacement decisions remain closely linked to infrastructure investment trends, logistics performance, electricity costs, and confidence in the broader investment outlook.

January 2026 vehicle export sales at 24 568 units reflected a year‑on‑year increase of 136 vehicles, or 0,6%, compared to the 24 432 units exported in the corresponding month last year. The export performance was supported by currency stability and easing imported input cost pressures. However, naamsa cautioned that the export outlook is increasingly shaped by heightened protectionism across several of South Africa’s key export markets.

Naamsa reflects that the proliferation of trade‑restrictive measures and evolving industrial policies in advanced economies continue to test South Africa’s automotive export competitiveness and market access conditions.

Furthermore, deepening trade and industrial arrangements between Western and Eastern economies, including preferential trade agreements, regional content rules, and strategic supply chain realignments, are expected to pose upward risks to South Africa’s vehicle export competitiveness and market share in certain traditional export destinations.

These developments underscore the growing importance of cost competitiveness and policy certainty in sustaining South Africa’s export performance over the medium to long term.

Looking ahead, naamsa emphasises that the industry awaits with pressing anticipation the finalisation of the comprehensive review of South Africa’s automotive policy framework, which is crucial for the sector’s long‑term competitiveness, investment attractiveness, and resilience.

In an increasingly complex and rapidly evolving global automotive environment, characterised by technological disruption, shifting trade alliances, and accelerated energy transition pathways, a coherent, forward‑looking policy framework remains critical to secure South Africa’s position within global and regional automotive value chains.

More results here: Vehicle sales January 2026

CFAO‘s Mc Duling Motors under the leadership Allan Stiles as Dealer Principal scooped the top award as Dealer of the Year at VW’s recently held Grand Prix Awards.

Nissan’s decision to drop a planned $500 million investment in electric vehicle (EV) production at its Canton, Mississippi plant is the latest indication that established manufacturers are reassessing how quickly the market will shift to battery power.

Donald Trump has threatened to increase United States (US) tariffs on cars and trucks imported from the European Union to 25% from next week, up from the 15% rate set under last year’s so-called Turnberry framework.

Advertisement

Advertisement

Advertisement

Advertisement

Have you ever noticed that anybody driving slower than you is an idiot, and anyone going faster than you is a maniac?

George Carlin

Donald Trump has threatened to increase United States (US) tariffs on cars and trucks imported from the European Union to 25% from next week, up from the 15% rate set under last year’s so-called Turnberry framework.

No, the Chinese are not coming to take over – they are already busy accomplishing it.

Motorists and households already under pressure will have to dig deeper into their pockets yet again from Wednesday, with sharp fuel and energy price hikes taking effect across South Africa.