CMS Systems marks 25 years in automotive retail technology

CMS Systems is celebrating 25 years in business, marking a significant milestone for a company that has become a central player in automotive retail technology.

- Industry News

- 24 April 2026

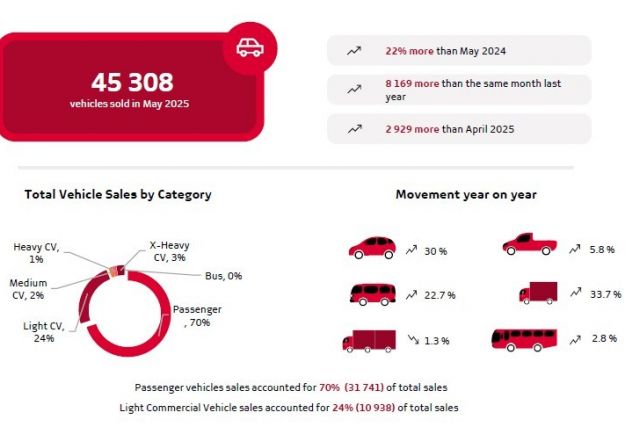

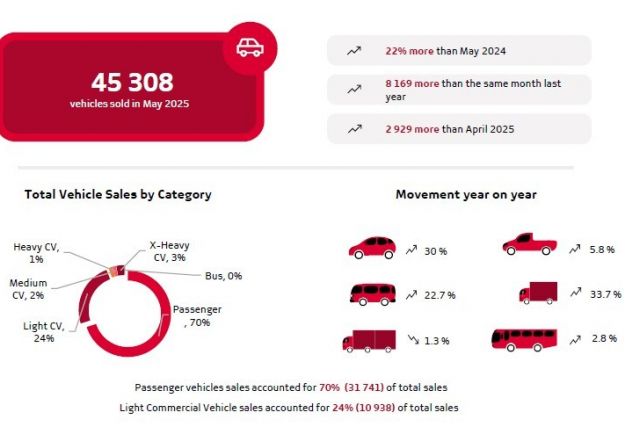

It is more good news about car sales for May with new-vehicle figures of 45 308 units, which reflected an increase of 8 169 units, or a substantial gain of 22.0%, from the 37 139 vehicles sold in May 2024, buoyed by relatively stable economic fundamentals earlier in the year.

Overall, out of the total reported industry sales of 45 308 vehicles, an estimated 40 062 units, or 88.4%, represented dealer sales, an estimated 6.8% represented sales to the vehicle-rental industry, 3.0% to industry corporate fleets and 1.8% to government sales.

The May 2025 new passenger car market, at 31 741 units, registered an increase of 7 322 cars, or a gain of 30.0%, compared to the 24 419 new cars sold in May 2024. Car rental sales accounted for 8.5% of new passenger vehicle sales during the month. Domestic sales of new light commercial vehicles, bakkies and mini-buses, at 10 938 units during May 2025, recorded an increase of 601 units, or a gain of 5.8%, from the 10 337 light commercial vehicles sold during May 2024.

Sales for medium and heavy truck segments of the industry reflected a sound performance in May 2025 and at 660 units and 1,969 units respectively, recorded an increase of 122 units, or 22.7% from the 538 units sold in May 2024 in the case of medium commercial vehicles and, in the case of heavy trucks and buses, an increase of 124 vehicles, or 6.7%, compared to the 1 845 units sold in the corresponding month last year.

However, not all indicators moved in the right direction. Vehicle export sales decreased by 5 165 units, or 14.6%, to 30 112 units in May 2025 compared to the 35 277 vehicles exported in May 2024. However, vehicle exports for the year to date were still 1.4% ahead of the same period last year.

The decrease in exports during the month could be attributed to a major exporting OEM halting production from mid-April to mid-May to complete the remaining 40% of the required installations and upgrades in its body shop, paint shop and final assembly areas in preparation for the introduction of a new model.

However, the fragility of global demand in the face of rising protectionism is increasing and highlights the importance of maintaining export competitiveness through policy alignment, market diversification and value-chain resilience, naamsa states.

View more results here.

CMS Systems is celebrating 25 years in business, marking a significant milestone for a company that has become a central player in automotive retail technology.

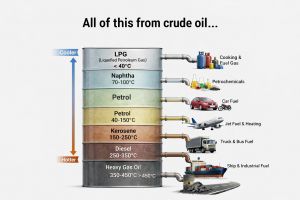

Oil prices jumped on Wednesday after Iran's seizure of container ships in the strait.

Hyundai Motor is preparing an aggressive comeback in China, unveiling plans to launch 20 new vehicles over the next five years as it tries to rebuild its position in the world’s largest car market.

Advertisement

Advertisement

Advertisement

Advertisement

Have you ever noticed that anybody driving slower than you is an idiot, and anyone going faster than you is a maniac?

George Carlin

CMS Systems is celebrating 25 years in business, marking a significant milestone for a company that has become a central player in automotive retail technology.

Oil prices jumped on Wednesday after Iran's seizure of container ships in the strait.

Hyundai Motor is preparing an aggressive comeback in China, unveiling plans to launch 20 new vehicles over the next five years as it tries to rebuild its position in the world’s largest car market.