BMW iX3 crowned World Car of the Year 2026 as EVs lead the way

The BMW iX3 has been named World Car of the Year 2026, with the announcement made at the New York International Auto Show on 1 April.

- Industry News

- 2 April 2026

While artificial intelligence (AI) investments offer substantial growth and profitability opportunities for insurance companies, they also introduce new risks that could significantly impact financial performance and credit ratings if not properly managed, according to Morningstar DBRS analysts.

Insurance companies have historically utilised machine learning, natural language processing and predictive analytics for underwriting models. However, AI-powered technologies have now become more widespread and essential for maintaining competitiveness.

Research by Wipro Limited reveals that North American insurers have increased their proportion of IT budgets allocated to AI technology from 8% in 2024 to more than 20% over the next three to five years.

AI provides significant advantages by enhancing operational efficiency through automating repetitive, high-volume tasks such as generating policy templates, summarising customer interactions and extracting key information from large datasets.

The technology also improves customer experience by identifying behaviour patterns and preferences, streamlining sales and marketing efforts, thereby reducing customer acquisition costs. Many insurers have deployed AI-powered chatbots and virtual assistants that simplify the complex insurance purchasing process by recommending policies based on individual preferences.

In property and casualty insurance, AI can assess vehicle or property damage using digital photographs and provide repair-cost estimates before physical inspection. It also expedites loss assessment during natural catastrophes by evaluating exposure to specific events more quickly.

Fraud detection represents another valuable application, with AI models trained on historical data identifying suspicious claims for further review while expediting payments for legitimate claims.

However, Morningstar DBRS warns that companies using AI assessments to reject claims could face legal and reputational risks if AI models prove unreliable.

The most serious challenges arise when AI is used extensively in underwriting and pricing policies, as these decisions directly impact profitability. Insurance companies could face costly errors and biases, particularly when quoting premiums for characteristics poorly represented in training data. Additionally, evolving regulatory landscapes could result in fines.

Smaller companies face particular challenges owing to underdeveloped frameworks, limited resources and restrictive data access, leading to potential decision-making errors.

While AI adoption is necessary for competitiveness, insurers must develop commensurate risk management frameworks. From a credit-rating perspective, AI can both enhance and damage franchise strength by affecting customer experience and operational risks.

The BMW iX3 has been named World Car of the Year 2026, with the announcement made at the New York International Auto Show on 1 April.

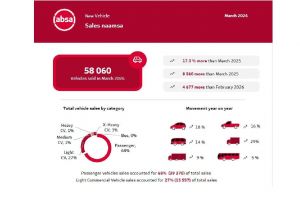

Retail new vehicle sales continue to surge in South Africa despite global and regional conflicts, local floods and droughts.

South Africa’s new vehicle market delivered a standout performance in March 2026, extending its domestic growth trajectory to the strongest level seen in nearly two decades.

Advertisement

Advertisement

Advertisement

Advertisement

You can't buy happiness but you can buy cars and that's kind of the same thing.

Unknown

The BMW iX3 has been named World Car of the Year 2026, with the announcement made at the New York International Auto Show on 1 April.

Retail new vehicle sales continue to surge in South Africa despite global and regional conflicts, local floods and droughts.

South Africa’s new vehicle market delivered a standout performance in March 2026, extending its domestic growth trajectory to the strongest level seen in nearly two decades.